National Treasury’s cuts on development spending plans have received a thumbs down from financial and economic analysts who have termed it ‘not growth-friendly’.

“A path where much of the burden of fiscal consolidation is disproportionately shouldered by development spending, as is the case in Kenya, undermines the underlying growth potential of the Kenyan economy,” said the World Bank in its 18th Kenya Economic Update (KEU).

“In this regard, there is a need to recalibrate the balance between development and recurrent expenditures, with the latter bearing a higher share of the expenditure containment.”

The World Bank says this can be through the lowering of transfers to state owned enterprises, cleaning and regular audit of the payroll register, keeping wages, salaries and allowance adjustments in line with

recommendations from the Salaries and Remuneration Commission (SRC) and maintaining frugality in operations and maintenance expenses.

Allen Dennis, World Bank Senior Economist says while progress is being made to advance the “Big 4”, given the ambitious nature of these objectives, “Achieving the Big 4 agenda would require much more expenditure reallocation to these critical sectors. It would be equally important for there to be improvement in efficiency of spending.

The Kenyan Government intends to increase its budget on infrastructure, education, health and social safety net and preparations for the elections the 2017/18 Fiscal Year.

The National Treasury’s ‘2017 Budget Policy Statement’ states that the areas outlined ‘remains a priority so as to realise benefits and maintain positive growth momentum, create jobs, reduce poverty and inequality.”

Financial and economic analysts have projected a positive outlook on Kenya with expectations of continued policy reforms reducing government debt to cut its soaring fiscal deficit.

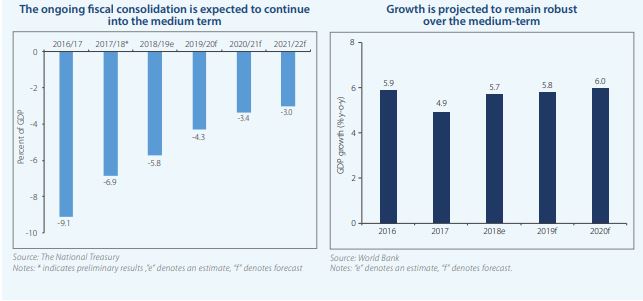

According to the World Bank, Kenya’s real gross domestic product (GDP) growth is projected to rise to 5.7% in 2018—up from 4.9% in 2017—and continue to increase steadily to 5.8% in 2019, and 6.0% in 2020.

The International Monetary Fund (IMF) projects a 6.0 percent in 2018. National Treasury projects an economic recovery with a similar growth from 4.9 percent in 2017.

However, Kenya is being advised to improve on its debt management.

IMF in its latest regional economic outlook for Sub-Saharan Africa report, says Kenya is vulnerable to currency and interest rate risks “This entails strengthening capacity to undertake a cost-risk analysis of borrowing options and manage repayments on commercial borrowing (Kenya, Uganda).”

On the other hand, the World Bank also notes “Debt management could be improved by rebalancing the mix of expensive and shorter maturity commercial debt with concessional debt that is more affordable and with longer maturity profiles.”

Currently, the CBK and Treasury have been continuously trying to ensure yields across the curve drop and remain below the maximum lending rate of 13.0%, partly to make a return-informed case for private sector lending.

“This may, however, prove difficult when the government comes back to the market for debt to finance its budget deficit. Appetite for longer dated papers has considerably waned partly due to pricing and the obvious mismatch between these tenures and bank liabilities.

Meanwhile, the shift back to T-bills by the greater market has seen significant shortening in bond maturity profile which considerably raises concentration risks for government in as far as debt servicing is concerned,” observes Faith Atiti and Stephanie Kimani,CBA Group Analysts.

The current national debt stands at 58% of the country’s gross domestic product up from 42.8% in 2008.

The World Bank also adds that developing the local currency bond market could spur significant interest from foreign investors and potentially reduce country borrowing costs, extend the maturity profiles of local currency bonds, and reduce exposure to foreign exchange risk.

Treasury says it will continue to strengthen expenditure control and improve the efficiency of public spending through public financial management reforms in order to free fiscal space for priority social and economic projects.

The adoption of the zero-based budgeting and a strict adherence to President Uhuru Kenyatta’s directive to freeze all new projects until completion of ongoing ones.

“This will improve efficiency of our public investment, streamline spending and reduce waste, ”The 2018 Budget Review and Outlook Paper (BROP).

Fiscal policy over the medium-term, Treasury says expenditures will decline gradually from 24.2 percent of GDP in FY 2017/18 to 22.0 percent of GDP in FY 2021/22 due to continued austerity measures instituted on less productive areas of spending across the Government.

“As a result, the overall budget is projected to gradually decline from the 6.7 percent of GDP (target was 7.2 percent) in FY 2017/18 to 5.7 percent of GDP in FY 2018/19, to 4.6 percent of GDP in FY 2019/20 and below 3.1 percent of GDP by FY 2021/22. This is in line with the fiscal consolidation programme that targets a deficit of 3.0 percent of GDP by FY 2022/23.”